Introduction

Auto insurance can feel like a fixed monthly burden. The bill arrives, you pay it, and life moves on. Yet premiums are not carved in stone. Insurers calculate rates using dynamic formulas built on risk signals, behavior patterns, and economic data. When you understand those variables, you gain leverage.

Saving money on coverage doesn’t require risky shortcuts or shady tactics. It demands awareness. Small adjustments—applied deliberately—can create meaningful financial relief over time. Think of it like tuning an engine. Minor calibrations improve efficiency without sacrificing performance. Let’s explore practical, completely legal strategies that can lower your auto insurance premium in measurable ways.

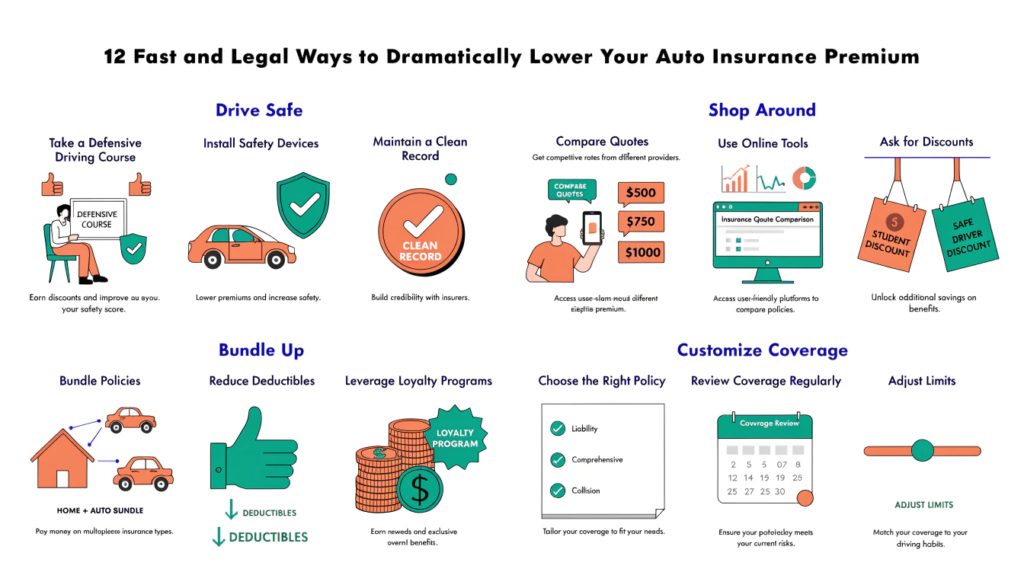

Shop Around With Purpose, Not Just Curiosity

Many drivers stay with one insurer for years out of habit. However, insurance pricing changes constantly. Companies revise underwriting guidelines, adjust claim projections, and compete aggressively for certain driver profiles.

Request quotes from at least three reputable insurers every year. Ensure each quote reflects identical coverage limits and deductibles. Without consistent comparisons, price differences become misleading. Even a $40 monthly gap equals nearly $500 annually. That’s not pocket change. Shopping strategically transforms market competition into personal savings.

Increase Your Deductible—But Calculate the Risk

Raising your deductible reduces your premium because you accept more financial responsibility in the event of a claim. For example, shifting from a $500 deductible to $1,000 often cuts collision and comprehensive costs noticeably.

However, don’t treat this as a blind cost-cutting trick. Ask yourself a simple question: could you comfortably cover that higher amount tomorrow if an accident occurred? If the answer feels uncertain, the savings may not justify the exposure. Smart budgeting matters more than marginal discounts.

Bundle Policies for Multi-Layered Discounts

Insurance companies reward consolidation. When you combine home, renters, condo, or life coverage with your auto policy, providers typically apply multi-policy discounts. These reductions often range between 10% and 25%.

Beyond savings, bundling simplifies administration. You manage fewer renewal dates and fewer service contacts. It also strengthens your relationship with one insurer, which may improve claims handling experiences. In many cases, bundling represents the fastest path to noticeable premium reduction.

Guard Your Driving Record Like an Asset

Your driving history acts as a financial fingerprint. Speeding tickets, reckless driving violations, and at-fault accidents send red flags directly into underwriting algorithms. Clean records, by contrast, unlock preferred pricing tiers.

Adopt preventive habits. Leave earlier to avoid rushing. Maintain safe following distances. Small behavioral changes dramatically reduce long-term insurance costs. Insurers reward consistency because consistent drivers file fewer claims.

Complete a Defensive Driving Course

Defensive driving courses refresh hazard awareness and sharpen reaction times. Many insurers offer discounts for approved course completion. These reductions sometimes last three to five years.

The cost of enrollment is usually modest. In most cases, total premium savings exceed the course fee. That makes it a practical investment rather than an expense. Additionally, the skills learned may prevent accidents altogether, which delivers long-term financial benefits.

Strengthen Your Credit Profile

In many states, insurers use credit-based insurance scores to assess risk. Statistical models show that individuals with stronger credit histories tend to file fewer claims. As a result, higher scores often translate into lower premiums.

Improving credit doesn’t require dramatic action. Pay bills on time. Reduce outstanding balances steadily. Avoid unnecessary new credit accounts. Over several months, responsible financial behavior can yield noticeable insurance savings.

Reevaluate Coverage on Older Vehicles

As vehicles age, their market value declines. If your car’s resale value drops significantly, maintaining full coverage may become inefficient. Compare the annual cost of collision and comprehensive protection against the vehicle’s current worth.

If coverage costs approach or exceed potential payout value, consider switching to liability-only insurance. However, weigh this carefully. If replacing the vehicle would strain finances, maintaining broader coverage may still make sense.

Drive Less, Pay Less

Mileage plays a powerful role in risk assessment. The more you drive, the higher your exposure to accidents. If your commuting habits change—perhaps due to remote work—inform your insurer.

Many companies offer low-mileage discounts. Even modest reductions in annual driving distance can shift you into a lower risk bracket. Accurate reporting ensures your premium reflects reality, not outdated assumptions.

Install Verified Safety and Anti-Theft Features

Vehicles equipped with anti-theft systems, immobilizers, and tracking devices present lower theft risk. Insurers recognize this and often apply discounts.

Before investing in new equipment, confirm eligibility with your provider. Not all devices qualify. When properly documented, however, safety upgrades can generate recurring premium reductions year after year.

Explore Usage-Based Insurance Programs

Usage-based insurance leverages telematics technology. A small device or mobile app monitors driving habits such as braking intensity, speed consistency, and nighttime travel frequency.

If you already drive cautiously, these programs may reward your behavior with personalized discounts. However, aggressive driving patterns could reduce savings potential. Review program terms carefully before enrolling to ensure alignment with your habits.

Remove Unnecessary Drivers From Your Policy

Household members significantly influence premium calculations. If someone listed on your policy rarely drives your vehicle or no longer resides in your home, review their status.

Excluding high-risk drivers—when legally permissible—can reduce overall exposure. Always confirm policy rules with your insurer before making adjustments to avoid coverage complications.

Conduct an Annual Policy Audit

Insurance needs evolve with life changes. Marriage, relocation, vehicle upgrades, or career shifts all impact risk classification. Failing to update your policy may result in overpayment.

Schedule a yearly review before renewal. Examine coverage limits, deductibles, and optional add-ons. Eliminating outdated protections prevents slow premium inflation over time.

Choose Future Vehicles With Insurance in Mind

Insurance costs vary widely by vehicle type. Sports cars and luxury models often carry higher premiums due to repair complexity and theft risk.

Before purchasing a new car, request insurance quotes for multiple models. A seemingly small difference in design can create substantial long-term savings.

Pay Premiums in Larger Installments

Monthly payment plans sometimes include installment fees. Paying semi-annually or annually may eliminate these charges.

Although upfront costs increase, total yearly expenditure often decreases. If cash flow permits, this adjustment can deliver immediate savings without altering coverage.

Maintain Continuous Coverage

Gaps in coverage signal instability. Even brief lapses may cause insurers to increase rates upon reinstatement.

Avoid cancellations unless absolutely necessary. Continuous coverage demonstrates reliability and supports favorable long-term pricing.

Conclusion

Lowering your auto insurance premium doesn’t require drastic measures. It requires informed adjustments and periodic review. Insurers respond to behavior, data accuracy, and risk management strategies.

By comparing quotes regularly, adjusting deductibles thoughtfully, improving credit, and maintaining safe driving habits, you convert insurance from a passive expense into an actively managed financial tool. Consistency creates compounding savings. Smart drivers treat their policy like an investment, not just a bill.

Frequently Asked Questions

How often should you compare auto insurance quotes?

You should compare quotes at least once per year, ideally 30 to 45 days before renewal. This timing allows sufficient opportunity to evaluate alternatives without rushed decisions. Additionally, compare immediately after major life changes such as moving, purchasing a new vehicle, or improving your credit profile.

Does raising your deductible always guarantee savings?

Raising your deductible usually lowers your premium because you assume more risk. However, savings percentages vary by insurer and claim history. Always calculate the break-even point. If annual savings equal only a small fraction of the deductible increase, the adjustment may not be worthwhile.

Can a defensive driving course truly reduce premiums?

Yes, many insurers recognize certified defensive driving courses. Discounts vary by provider and state regulations. Besides direct savings, improved driving skills reduce accident probability, which protects your record and supports lower rates long term.

How does credit influence insurance pricing?

In states where permitted, insurers use credit-based scoring models. These models correlate financial stability with claim likelihood. Responsible credit management often leads to lower premiums. However, certain states restrict or prohibit this practice.

Is usage-based insurance safe and private?

Usage-based programs operate under regulatory oversight. Insurers collect driving data primarily for pricing evaluation. While privacy policies vary, reputable providers disclose data usage clearly. Review terms carefully before enrollment.

When should you drop full coverage on a vehicle?

Consider dropping collision and comprehensive coverage when annual premiums approach 10% or more of the vehicle’s market value. However, evaluate your financial capacity to replace the vehicle outright before making changes.